Steve asked:

I have received £4000 from a payday loan refund. I have a £2500 loan with Amigo, £1500 left on a Likely Loans loan, a £2000 overdraft and 750 x 2 on credit cards. (Limit 800 on each). My dilemma is not knowing how to spend the £4000 in order to boost my credit score. Which is the most damaging and needs paying first?

Although your situation won’t be the same as Steve’s, you may be interested in finding out what sort of things matter when deciding what debt to clear first.

As I don’t know anything else about Steve’s situation, I am going to make the big assumption that paying off the debts he mentions really is his top priority. If he had priority debts or bills such as rent arrears or council tax, they should be his main target.

How to improve Steve’s credit score

Steve is asking which debts to clear to improve his credit score. He probably has a poor credit record, otherwise he wouldn’t be in such mess, having to borrow from Likely Loans which typically charge a horrible 60% or expensive guarantor loans such as Amigo – where 50% is the typical interest rate.

If he has defaults, missed payments or CCJs on his credit record, paying off some of his high-cost debt is a great idea for his finances, but it isn’t going to improve his credit score much. If there are “bad things” on your credit record, clearing some debt doesn’t normally have much effect.

A lender you apply to for more credit can’t see what other lenders you have already borrowed from. They can see what sort of debt it is – whether it is a loan, a high-cost short-term loan such a payday loan, a credit card/catalogue account or an overdraft – but this doesn’t directly affect your calculated credit score. Some lenders, especially mortgage lenders, don’t like you to have had payday loans in the last year.

One area where it is possible to boost your credit score is if you can get credit card balances down. You are hit with a credit score penalty if your balance is over 90% of your credit limit, and this applies to both Steve’s credit cards. And you get a boost to your score if your balance is under 30% and a bigger boost if it is actually zero!

Going forward the best thing for Steve’s credit score is going to be to clear both credit cards and then use them each for something small each month, a tank of petrol say – then repay them in full.

But credit scores aren’t the only thing that matters!

Steve has probably lived with bad credit for a long while. But the most important thing to do with this windfall money is to use it to improve his long-term finances, and for that his credit score is only a small part of the picture. Two other things matter much more:

Paying as little interest as possible

If Steve pays off his highest interest debt first, then he will have more money left each month to repay his other debts. If you can clear A then B then C within 9 months, that’s better than clearing B then C and A still being there in a years time.

So Steve needs to find out the interest rates on each of his debts. For the loans this is straightforward. For the credit cards it will be on his latest statement, but be careful if it sounds low – they may be quoting a monthly rate not an annual one… There is a calculator here to help.

Many banks have complicated overdraft charging structures. Steve needs to look at what his overdraft charges were last month – it’s quite likely they were high so tackling the overdraft is really important.

Getting rid of “difficult” debt

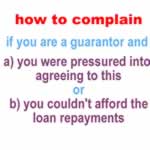

I always suggest that guarantor loans and logbook loans should be the top priority to clear as they can cause so many problems if you get into financial problems. If I were Steve, that Amigo loan would be the first one I would clear even if some of his other debts are higher interest – it will be great to know that his guarantor is no longer at risk even if he loses his job.

Overdrafts are also very difficult to escape from – you may pay a chunk off one month but the next month it is just run up again. Steve should take advantage of his poor credit score to open a basic bank account and switch to using that as his main account. From here on his old overdraft is just another debt to be cleared and if he pays in more than the overdraft fees are each month it is going to start dropping.

More affordability complaints

He should also look at whether he can get refunds from Amigo and Likely Loans. if he has had payday loan refunds, then Amigo and likely loans may not have done enough checks that their loan would be affordable.

Readers are having a lot of sucess with affordability complaints against Amigo recently, see how to complain if you are the borrower for a guarantor loan. And also winning affordabilty complaints againt the large loan bad credit lenders such as 118 money, Avant Credit, Everyday loans and Likely Loans.

A possible plan for Steve

So a possible plan for Steve could look like this:

- clear the Amigo loan and the Likely Loan with the £4,000.

- put in affordabilty complaints to Amigo and Likely Loans.

- open a new basic bank account.

- take the money he was paying to the Amigo and Likely Loans each month and divide it between the 2 credit cards and his old abandoned overdraft.

- when the credit cards get down to zero, keep them open (good for his credit score!) and use them each month and repay them in full each month.

Complaints by the guarantor for a loan

Panorama program covers guarantor loans

How to ask for a payday loan refund

Leave a Reply