A reader asked:

I moved in with my parents into their council house several years ago and we are looking into the right to buy scheme. We received the paperwork and it stated that you are not entitled to the right to buy if you owe money to creditors.

Five years ago I lost my job and had a relationship breakup and unfortunately got into debt. Two accounts were defaulted and I went into a payment arrangement with them. I have maintained the payment agreements and gradually increased them but still owe quite a bit (£5,000) on the credit card.

I am back in work now. I have been offered full and final settlements – will this mean my debts are paid in full and I can then go ahead with the council house purchase? Or will I need to pay the outstanding debts in full for this to be classed as ‘owing no money to creditors’?

I know that getting a mortgage is still going to be an issue however :(

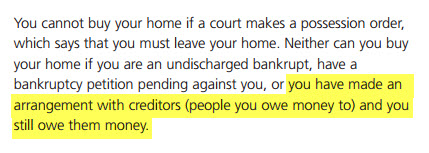

The Right to Buy provisions about debt

I have highlighted the relevant part of the Right To Buy rules (if you are looking at your council’s information sheet, the layout may vary but it should say much the same):

This may sound as though it applies to you – after all you have made an arrangement with your creditors and you do still owe them money. However the good news is that it doesn’t!

The type of arrangement this paragraph is referring to is is an Individual Voluntary Arrangement (IVA) which is a formal legal contract with your creditors. It is a type of insolvency, like bankruptcy.

It doesn’t apply if you have an informal arrangement with your creditors. This happens if you have made an agreement with each creditors yourself or if you are going through a debt management firm and are in a Debt Management Plan (DMP).

So the reader’s arrangements with her creditors won’t stop her being able to use the Right To Buy with your parents.

If you are wondering why it matters if you are in an IVA but not a DMP, it’s because buying a house means that you are acquiring an asset, and that would cause all sorts of legal problems if you were in a form of insolvency such as an IVA, so the whole option is being ruled out. These sorts of legal issues just don’t arise with a DMP.

Getting a mortgage

But even though these debts won’t prevent you from exercising your Right to Buy, they are very likely to mean it’s very hard to get a mortgage offer. This is for two reasons:

- the defaults on your debts mean that your credit record won’t be good, and

- you still owe money, which will worry a lender.

Both of these factors will make it harder for you to get a mortgage – you may find Can I get a mortgage when I am in a DMP? useful reading.

Using a full and final settlement to clear the debts is probably a very good way forward for you – it solves the second problem completely and by changing the balance owed to zero, your credit record will also start to improve.

As the defaults will have been a long while ago (at least they should be – if they are not at least four years ago have a look at whether the default date is correct and if it isn’t, get it changed) this may well be enough for you to get a mortgage later this year. With any problems on your credit file at all, it’s always worthwhile going through a broker, not direct to a lender.

Be sure a mortgage is right for you

It may feel like a no-brainer to buy the house at such a huge discount, but three things to think about:

- if you have more work problems it is much easier to get help with rent through Housing Benefit / Universal Credit than it is to get help with mortgage payments;

- investigate in detail any service charge you may have to pay the council – people can find themselves landed with surprisingly large bills after a few years that they can’t afford;

- think what will happen if you decide you want to move out, perhaps you have a new partner or your job moves. At the moment your parents have a secure home for life.

Faz says

I have an IVA setup through step change, I have been on this plan for a year and have 4 more years to do. I was unable to continue to work full time due to ill health. However my partner is working full time and we both have lived in the same house for over 10 years and both our names are on the tenancy agreement and want to do the right to buy. Would we still be able to do the right to buy even though I am on the IVA and not my partner. I have contacted a broker who said he will be able to help but I am worried if I will be offered the right to buy due to my credit history. Please help with any information on how to proceed.

Sara (Debt Camel) says

So far as I know the information in the above article is still correct – you can’t use Right To Buy if you are in an IVA. I suggest you do not pay any fees to a broker who says he may be able to get you a mortgage, it isn’t the mortgage here that is the problem, it is the RTB rules.

Can I ask how much you are paying each month to the IVA? And why if you don’t have a house with equity you did not opt for bankruptcy instead?

Jeffrey Yaw says

I am currently in an IVA and planning to make an application to buy my council property with the right to buy discount scheme. I read the earlier reply which stated that while in an IvA i may not be entitled, can i ask what if i make a final offer to clear the IvA with the help of my partner. Once the IVA is settled would that be deemed ok for me to proceed to make my application as it will be settled, thank you and i look forward to your reply.

Sara (Debt Camel) says

If your IVA has been completed it will probably be OK with the Council. But with an IVA on your credit record you will normally find it impossible to get a mortgage, and that applied even when the IVA is completed.

Jeffrey yaw says

Thank you for your reply, i am aware and currently in talks with a company who could help. Will they see an early settlement same as being completed? Because with early settlement it still stays on your record till the full period, will that be an issue with the council or the fact it is settled early will be enough to meet the council’s criteria? Thanks

Sara (Debt Camel) says

You would need to ask the council this.

kerry says

Hi, I’m nearly comin to the end of my iva, and I was wondering would a family member be able to buy my council home for me in 1 full payment as my nan has offered to buy my house for me and my children in my name.

Sara (Debt Camel) says

That probably isn’t possible and even if it was, it would be a VERY BAD IDEA until your IVA has ended. Because your nan (sounds a lovely lady!) would be giving you a large gift of the money and your IVA company would insist you used that to repay all your debts in full.

You need to wait until your IVA has finished and you have your completion certificate. Then your nan can give you the money and you can buy the house.

Shelley Barnes says

I am looking at the options to help my right to buy for paying off my debts with a potential small win fall. Due to mental ill health our family fell into financial difficulties and had a repossession on our home with outstanding balance, dated 2017 I also have 3 CCJs last one dated 2019 (due to me missing the letter). I am at this stage not worried about the mortgage but just want to know for the right to buy would I qualify if I partly settled my CCJs and the old mortgage and I have no other creditors I owe to or would I only be able to buy if I had fully settled these 4 debts?

Sara (Debt Camel) says

It’s pretty unlikely you can settle recent CCJs cheaply.

Right to buy mortgages are a very specialist area, you need to talk to a broker that covers this niche to see if you can get a mortgage with 3 recent CCJs even if they are settled in full.

Leanne says

Will 1 CCJ from 4 years ago mean I am not eligible for the right to buy scheme

Sara (Debt Camel) says

No, but it may mean that it is hard to get a mortgage. Has the CCJ been repaid? Do you have defaulted debts as well?

Leanne says

Hi, thanks for the reply. I will not require a mortgage as it will be paid full in cash

Elaine says

Are you able to have the RTB if you have a 4 year old unsettled default? There is no arrangement to pay in place and nor has there been and as far as I can see, the RTB legislation only states you can’t have the RTB if you have any “composition or arrangement in place, the terms of which remain unfulfilled.”

Does having old personal loans that weren’t repaid actually prevent you from being able to have the RTB even though there are no asset-based legal issues with this?

Sara (Debt Camel) says

It won’t prevent you from buying under the RTB scheme. But it may mean that lenders will not give you a mortgage at a reasonable rate. Has the debt been sold to a debt collector?

Elaine says

Yes it has been sold to a debt collector but I already have a full mortgage offer in place as the debt is over 4 years old so they were happy to lend. It’s the Council interpreting the clause as any debt whatsoever, even if there are no asset-owning legalities to consider. An old personal loan debt is irrelevant to assets that you own and I’ve already confirmed I am in no IVA or any arrangement whatsoever with the creditor; no bankruptcy, no nothing.

John Robson says

Hi my partner has a DRO and I (partner) just been. Added to rent book and want to buy council house with her. I have sold my previous property and have the funds to buy cash. Will/would it be a problem? I no this may sound harsh but theses debt were from her previous relationship and being incredibly stupid running up debt so I refuse to be held responsible for negligence with debt before I met her. I love her but her debt is her debt and her DRO will be finished in 10 months. So after that would we be able to purchase council house ?

Sara (Debt Camel) says

You are under no obligation to clear her old debts. If you were living with her, then the debt adviser will have considered this when setting up her DRO. When the DRO is finished, you can talk to the council about buying the house – as you have the cash her poor credit raring will not be relevant for a mortgage.

Louise says

Can I get RTB with council with a recent ccj on my name? No mortgage will be required as my late fathers estate will pay for the house

Sara (Debt Camel) says

The article above highlights a provision in the RTB rules – so far as I am aware this does not cover monthly payments to a CCJ.

Are you actually making payments to the CCJ?

Louise says

Sara I only just found out about it as it was made to my file some 12 months after I moved house so atm no but I don’t have any information about it

Sara (Debt Camel) says

see https://debtcamel.co.uk/unknown-ccj-credit-record/

Leanne says

Hi Louise,

If it helps, I was in the same position as you. My house went through fine. Good luck!

Louise says

Thankyou ❤️

Haila says

I have a Ccj that’s been paid of.a few years ago and is due to come of my credit file would I be able to have the right to buy my council house

Haila says

Sorry I forgot to add it’s not off till end of next yer

Sara (Debt Camel) says

Having a CCJ on your record should not be a problem for exercising your right to buy. See the comments just above this one.

But it may be a problem for getting a mortgage. You need to talk to a mortgage broker about this.

Claire says

I have a DRO, its currently in the 12 months period from august all debts will be wiped will this stop me from buying my council home?

Sara (Debt Camel) says

In theory you can buy after your DRO has finished in August. But if you need a mortgage that may be difficult.

Liam says

Hi, i have a BRU that ends 18th July 2023 (1 week today). I applied for the RTB 3-4 weeks ago and i have now received a decline letter from council solicitors to say due to bankruptcy i am an unsecured tenant. Will i automatically be a secured tenant once my BRU has ended and can i re submit my RTB application next week immediately?

Sara (Debt Camel) says

due to bankruptcy i am an unsecured tenant

That is an unusual phrase to use. I suggest you go to your local Citizens Advice and ask for their help with this.

T.D says

My council have asked for circumstances surrounding a large overpayment of benefits from DWP. I have a payment plan in place and never missed a payment. I have savings and could make a substantial payment towards it. I don’t have an IVA or DMP so this won’t effect my eligibility for Right to Buy, but could the circumstances surrounding it? (I don’t have a very good understanding and was misinformed by my late husband and there is a language barrier too (I am deaf)).

Sara (Debt Camel) says

I think you should talk to your local Citizens Advice about this request and how to reply to the council. Also whether you should be trying to clear this overpayment faster.

Alexandra says

Hi there, What if you are in a joint IVA which is now half way through the term. Would it be possible to apply for the ‘Right to Aquire’ scheme? We’re housing association not council tenants.

Sara (Debt Camel) says

I don’t think so. Ask your housing association. Also you would find it extremely hard to get a mortgage.

M John says

Hi, i would like to buy my ex council property which is now housing association. However almost 6 years ago I had DRO, at the moment it is still on my credit file. My question is, after 6 years when it comes off my file would this affect my right to buy in any way? Ive lived at the house 15 years after exchanging with previous tenant of 20 years

Sara (Debt Camel) says

I think you could use the Right to buy now as your DRO has completed. But it will be easier to get a mortgage when it is off your credit record

Magdalena says

Hi.

Please I need help and advice in my situation.

I have had an IVA on my own name since June 2017 till June 2022. It’s settled and I’ve got a certificate of completion. It’s been 6 years on my credit file but now I am 2 years after my IVA . My IVA isn’t showing on my credit file anymore.

Do I have a chance to apply for a RIGHT TO BUY scheme for my council house that I am renting from council since 2010?

Plus I have to mention that the council tenancy is on my and my husband’s name and we would like to buy as a joint application . He didn’t have an IVA but had some missing payments on his credit file in 2019-2020. But since then we are no longer missing any payments.

He has credit card balance of : £118.89

Creation loan with balance of : 429.60

Currys my plan with balance : £816.49

Plus eon energy plan with balance £1213 ( but we are now only owe £665.72 as are half way through with clearing the balance and it shows on credit file still but we never missed any payments. They are just debts that we have and they are shown on credit history but we are paying them off on time .

Can we get RIGHT TO BUY chance to buy ? Or do we have to pay all the debts off first ?

Are we not allowed to have any kind of debt to get Right to buy or these need to be paid on time ?

Do we still got a chance to get joint mortgage with in this situation?

We are planning to pay all the debts off in couple of next months time to be debt free .

Sara (Debt Camel) says

A completed IVA no longer on your credit record shouldn’t be a problem for right to buy.

You don’t have to clear all your current debts before getting a mortgage, but they will affect whether the lender considers the mortgage is affordable. Having energy debts, which are a priority debt, is often seen as an indication you are in difficulty.

Magdalena says

Thank you very much for your reply.

Regards to the energy debt this is something that we didn’t have impact on because what happened was :

Eon was merging with Eon next and therefore we were not able to top up our meter because of some chances in the system ( we are on pay as you go scheme ) they didn’t let us to top up because of the error and we’ve tried to ring the many times to make a payment on the phone but weren’t able to . They’ve never cut our supply off, never sent us any letters asking for payments. They simply said that because of the situation with changes in the system we just need to wait for the final bill and are unable to top up at the moment until it’s all sorted.

After a year we had a big bill to pay , to clear the balance off and we couldn’t afford it to pay it in full and they’ve added £7 to each week top up to pay it off and now we’ve got £665 still to pay. This is is our credit file shown as NR. What is this mean then ? Are we in bad situation because of this ? I’ve rang them and explained that we are in the credit file reported with this and it doesn’t look good but they’ve said not to worry as it isn’t our fault and they will write this off soon as we will pay the balance in full .

So shall I worry or not do you think?

Sara (Debt Camel) says

I think you need to talk a mortgage lender about this – Right To Buy mortgages are pretty specialised and there is little point in me guessing.

Magdalena says

Also I would like to know if I have to tell about my previous IVA to the right to buy application?

The question on the application is:

Do you have an IVA agreement? It doesn’t say did you have in the past or something so I don’t know what to do ? Shall I answer : no? Because I don’t have an IVA at the moment. My IVA started in 2017 and settled in 2022. I’ve got a completion certificate and this was two years ago . I am worried if I will mention to the council that I had IVA in the past they might decline me straight away. What shall I do ?

Sara (Debt Camel) says

Do you have an IVA agreement?

No you do not.

If they had wanted to know if you had ever had an IVA, they should have asked that question.

Magdalena says

Thank you very much for your help. I really appreciate it.

I’ve been following your website since I had my IVA and this is really amazing that you helped so many people with your knowledge. Thank you so much !

Yvonne says

Hi I am going through a DRO and my daughter lives with me. My name is on the tenancy. How long do I wait until I can apply for the right to buy after my DRO.. can my daughter but the property or will I lose my discount.

Sara (Debt Camel) says

You can apply after your DRO year ends. But if you require a mortgage that is likely to be very difficult with the DRO on your credit record for another 5 years.

Your daughter cannot buy the property if the tenancy is in your name, it would have to be joint with you.

Nnanna says

Hi Sara , I have been denied RIGHT TO BUY by my council due to CCJ, the denial letter stated that Hosuing Act of 1985 states the following: The Rightto

belongs has made a composition or arrangement with his creditors the

terms ofwhich remain to’be fulfilled, I have no knowledge of this CCJ. Please I have read your comments on here, can you advise me on what to do, the stated that I have no right of Appeal, I think this is wrong

Sara (Debt Camel) says

You can make a complaint to your council and you should (I think) be able to take to to the Local Government Ombudsman (https://www.lgo.org.uk/) if the complaint is rejected. the LGO will say if the complaint has to go to the Housing Ombudsman instead.

Your local Citizens Advice may be able to help with this.

Noma says

Please may I have the relevant legislation interpretation relating to the type of ‘composition or payment arrangement’ referred to on the right to buy qualifying criteria. I need to evidence that this refers to formal contracts like IVA as stated in your previous post please.

Thank you

Sara (Debt Camel) says

The legislation is here: https://www.legislation.gov.uk/ukpga/1985/68/part/V 121(2)

I have given the standard interpretation of this. A composition is an arrangement negotiated with several creditors to pay them less. If you think your council is mis-interpreting this, I suggest you get help from your local Citizens Advice.

Noma says

If I had an arrangement to clear rent arrears of less than £300 with the council can this be used to reject an application for RTB please? Just that one informal arrangement and no other?

Sara (Debt Camel) says

I don’t think I have ever seen anyone try to exercise their right to buy when they owe the council money.

Will you be needing a mortgage? Because getting rent arrears suggests a mortgage may be problematic?

Mike says

This was part of my complaint to my council right to buy team and i also copied council complaints team for there record.. Am waiting for there update, will be updating here if it was rejected or accepted. I also inform them that I am willing to go to housing ombudsman

I have No Composition or Arrangement with Creditors:

Under Section 121AA of the Housing Act 1985 which explicitly states that a person cannot exercise the Right to Buy if they have entered into a formal composition or arrangement with creditors, and the terms of that arrangement remain unfulfilled and is not the case in this circumstance. A CCJ does not, in itself, constitute such a composition or arrangement. “A composition agreement is a voluntary arrangement, typically under the Insolvency Act 1986, whereby a debtor negotiates with creditors to settle debts for less than the total amount owed, usually under a binding agreement such as an Individual Voluntary Arrangement (IVA) and again this is not applicable in the case.”

The fact that I was unaware of CCJs at the time of my application further underscores that no arrangement or negotiation had been made. I contend that it does not imply that I entered into or failed to fulfill a composition agreement .Upon learning of these CCJs, I promptly resolved it in full.

Mike says

I have today been given the right to buy my flat , council accepted that CCJ is not a composition agreement. Thank you the team of this site , your information was a life saver for me. Thank you

Noma says

What is the process of assessing an application for RTB? Can the council start investigating former/previous landlords to determine % of discount to award a RTB applicant, before actually assessing if the application meets all the criteria to qualify for RTB?

Also are the council workers not bound by law of equity to act in a fair and just manner, where they should not sit and hold back information in order to disadvantage their tenants or to aid or influence certain outcomes that then disadvantage the public? This is in relation to the council responses especially just before the deadline of 21 November 2024 when the RTB laws changed

Sara (Debt Camel) says

I think it may be easier to say why your council has rejected your application rather than ask about generalities

Emma button says

Hi, can anyone help

I have been denied my RTB due to an IVA

I applied to complete my IVA on the 30th May 2024 due to back and forth it wasn’t paid in full until January 10th 2025 – I received my denial letter on January 14th 2025 – the have refused me an appeal

I have wrote to them and told them it’s paid and also presented a letter from the credit company to say it’s been paid and they have still refused me – what should I do next

Sara (Debt Camel) says

Are they saying you are currently ineligible? Or that you would only get the lower discount that came in late last year?

Linda says

Hi

We applied for right to buy within the previous time scale to be eligible for the previous right to buy discounts. Our application was refused and the denial was based on that we have a ccj. The application was joint with my partner who actually does not have any ccjs.

Their reply to my our complaint …..

“…. your application was denied on the basis that you had an unfilled financial obligation, a CCJ which has not been settled.

“As you have highlighted, under the provisions of section 121 of the Housing Act 1985, the Right to Buy cannot be exercised if the tenant has a bankruptcy petition pending against him/her, is an undischarged bankrupt, or has made a composition or arrangements with his/her creditors, the terms of which remain to be fulfilled.

It is the Ministry view that the tenant would not be eligible for the Right to Buy where he/she has an outstanding County Court Judgement against him/her or has a composition or arrangements with creditors which remain to be fulfilled. The tenant would be eligible for the Right to Buy once the County Court Judgement has been lifted and/or the terms of the composition or arrangements with creditors has been fulfilled”

Based upon the above information, I have not upheld your complaint, as I have not found any service failings.”

Can you help me to figure out how best to make a further complaint or where else to go with my complaint.

Sara (Debt Camel) says

Can you ask them to clarify where “this Ministry view” is published, as a CCJ is not a composition or arrangement with creditors.

If that doesn’t get anywhere, i suggest you ask your local Citizens Advice for their help.

Linda says

Hi Sara

Their response was structured as follows:

We have sought advice from the Department for Levelling Up, Housing, & Communities (DLUHC), the government agency that provides impartial advice on the Right to Buy. You can contact them by: Emailing enquiry@righttobuyagent.org.uk and Calling 0300 123 0913.

Their response is as follows;

“As you have highlighted, under the provisions of section 121 of the Housing Act 1985, the Right to Buy cannot be exercised if the tenant has a bankruptcy petition pending against him/her, is an undischarged bankrupt, or has made a composition or arrangements with his/her creditors, the terms of which remain to be fulfilled.

It is the Ministry view that the tenant would not be eligible for the Right to Buy where he/she has an outstanding County Court Judgement against him/her or has a composition or arrangements with creditors which remain to be fulfilled. The tenant would be eligible for the Right to Buy once the County Court Judgement has been lifted and/or the terms of the composition or arrangements with creditors has been fulfilled”

I therefore am left dumbfounded at their continued effort to quantify a ccj as a composition agreement.

Sara (Debt Camel) says

Well you can take an appeal to the Local Government Ombudsman. But you may prefer to get help woith this, which is why i suggested your local Citizens Advice

Peter says

Hi Linda

Which Council are you dealing with? I have not seen anywhere that the DLUHC have published their view on this.

Linda says

Hi

I am dealing with London Borough of Havering.