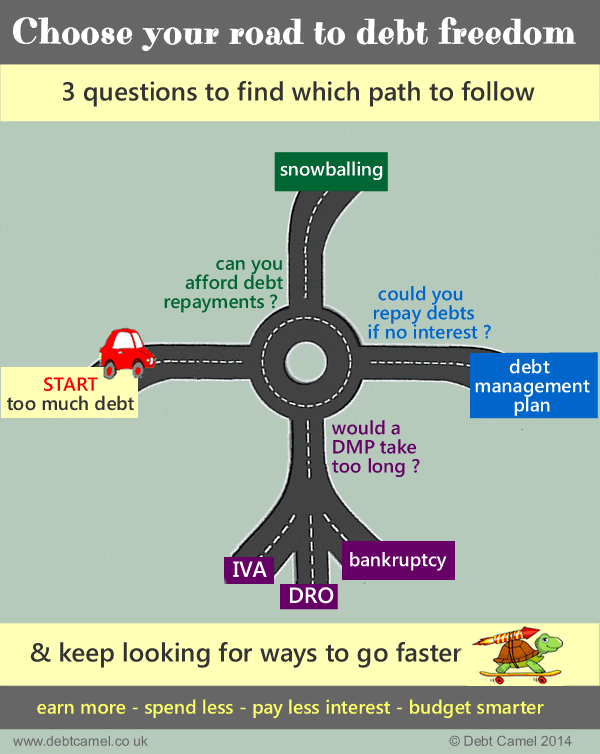

Go round the roundabout…

The picture at the top of this page is a good at-a-glance guide to handling problems with consumer debts such as loans, credit cards and catalogues.

Go round the roundabout and turn off at the first road that will work for you!

If you have priority debts including such as mortgage, rent, council tax or car finance arrears, these need to be handled differently, see Priority and non-priority debts.

The common debt solutions

The five main debt options are:

- Snowball your debts! Usually the best solution if you can make at least the minimum payments on your debts each month and your debts are falling, not increasing. As you snowball, your credit rating will get better and better, unlike all the other debt solutions that will damage your credit rating.

- Debt Management Plan (DMP) where you pay less than the normal payments each month and your creditors freeze interest – they almost always do.

This can just be a temporary measure if needed eg until you find another job.

The payment can be as little as £1 a month – these token payments aren’t a debt solution, just a holding measure. - Debt Relief Order (DRO) is often the perfect option if you owe less than £50,000, can pay less than £75 a month to your debts and don’t own a house.

- Individual Voluntary Arrangement (IVA) can work well if you have a reliable income and assets to protect such as a house with equity. Avoid if you have no assets to protect because a lot of IVAs fail and bankruptcy would also be cheaper.

- Bankruptcy which sounds scary but for many people it is the fastest and simplest way to be able to start again. Find out the facts rather than dismissing this because of myths and rumours that may not be correct for you.

The last three – DROs, IVAs and bankruptcy – are all types of insolvency. They are formal legal arrangements that aim to resolve a debt problem completely and are not suitable as a temporary measure. Most types of debt are included, but check this page for details.

There are three less common debt solutions:

- Full & Final Settlements These can be very useful if you have been on a DMP or haven’t been able to make any payments at all for a while and you may be able to get a lump sum.

- Write-off Debts, Creditors won’t usually consider these unless there are unusual circumstances, and

- Administration Order These are now extremely rare, you have to owe less than £5,000 and have a CCJ. If you think you would qualify, talk to a good debt adviser.

Affordability complaints

If you have been given unaffordable credit, look at asking for refunds:

- loan repayments may have been so large that you were left short and had to borrow more

- a credit limit increased on a credit card or catalogue when you had only been making minimum payments for a long while, or had been making a lot of cash withdrawals

- overdraft limit increased stupidly high when the bank should have seen you were already in big difficulties? You can complain about a student overdraft after the bank has started charging interest on it.

These may sound great! But it can be hard for you tell how good a case you have. Lenders reject many good complaints so they have to go to the Financial Ombudsman, which can take a long while.

So if you are in immediate difficulty, then often a good combination is a debt management plan, to get you into a safe financial space and affordability complaints, which will speed up the DMP if you win any.

Other ways to improve your situation

There are other ways to improve your finances , such as selling assets, paying less interest, reducing your expenses and increasing your income. If you can make a big enough change to your situation, then you may be able to snowball and not need a DMP or insolvency at all!

If you don’t have enough money for your expenses if you pay nothing to your debts, then this needs to be tackled before trying to resolve your debts, even if your debts feel urgent. Talk to a debt adviser as soon as possible.

Making the right choice

Choosing the best debt solution is vital. If you have read through how some of your possible options work, you will hopefully have ruled some of them out, but many people will feel unsure which of two options to choose.

Have a look at the Hard Choices page. That provides a direct comparison of many of the options, such as “IVA or bankruptcy”, and also looks at difficult decisions such as “How far should I cut back my expenditure?”

Good places to get debt help

Good, reliable and free debt help and advice is available.

- Make sure you talk to one of the good guys, for example a national charity such as National Debtline or your local Citizens Advice.

- The adverts you see offering “free advice” usually turn out to be anything but free… and never trust anyone that cold-calls you offering debt advice.

It’s important to take your time and research your options.

Don’t let worries about defaults or bailiffs panic you into making a fast decision that you will later regret. Good debt advisors want you to be comfortable with the route you choose and will be happy to answer questions about all the alternatives and how they work.

Ben says

I’m asking for my new partner she is separated

both her and her ex husband are with step change hes applied for a DRO 2 of the debts are joint she struggles to pay step change now but she is keeping up with her repayments he is picking and choosing when to pay step change does the insolvency agency need to contact her to inform her that her ex partner has applied for a DRO due to it being a joint debt.

Sara (Debt Camel) says

“does the insolvency agency need to contact her to inform her that her ex partner has applied for a DRO due to it being a joint debt.” no – but she knows anyway, so why does this matter?

If she is struggling, perhaps she should be looking at her other options? I suggest she talks to StepChange about this – she should have her DMP separated from his DMP and have her situation reviewed.

Jennifer says

Hope ur ready for this.

I have dept of £19000

My husband £16000

Joint £1000

He earns a wage of £1600

I don’t work as have 4 children 1-12 years. We get UC £1000 and child benefits £200 roughly.

I was told to get IVA of £110 Each

I have been told we cant do dro as dept is too much. However my husbands defo isn’t. I was told that the benefits would be included in the incomings which means he was over £50. Is this true? Or is it just his income if I go ahead with bankruptcy/ IVA too. I was told he would be treated as a single person so less allowance for expenses yet he isn’t and still in a family of 6.

Also if I went bankrupt, would his wage be included in income or just the benefits? Baring in mind he would be on a DRO.

So basically

Who’s money is included for individual cases?

Sara (Debt Camel) says

“I was told to get IVA of £110 Each” who told you this?

It sounds like an IVA firm… I think you both need better debt advice on your options, I suggest your local Citizens Advice or phone National Debtline on 0808 808 4000

Samantha says

Hi me and my Mum are looking for advice, we are both currently in DMP plans through StepChange. I am out of work long term due to mental illness, but my Mum is still trying to get work. I owe around £17,000 where as my mum’s is only around £11,000 (credit cards/loans)

I currently pay £70 and my mum is paying £60 a month, we are wondering if the DMP is best solution long term? as it’s going to take more than 10 years for both of us to clear the debt.

My Mum has a private pension pot from working with the NYCC, which currently sits undrawn, but she’s concerned if we consider insolvency options she may loose it? what are the options here please for us to consider for clearing this debt?

Sara (Debt Camel) says

How long has the DMP been going for?

How old is your mum?

Are you renting, is the tenancy in her name or joint? private rented or council/housing association?

Samantha says

Hi thank you for he reply we’ve had it for about a year but it will take over 10 years plus for both to clear I think mine works out at 19 and my mums is 15 years

We are not renting as we live at my Dads address which is housing association and the tenancy is in his name we are trying to move but it’s difficult with us being on benefits and we’re too low priority on local housing list.

Sara (Debt Camel) says

does your Dad live there or has he moved out and you can just stay there? The reason I am asking is it is a lot harder to rent privately if you have had a debt releif order in the last 6 years.

Insolvency is obviously an option for you if you are long term out of work because of mental health problems. That can never be affect your mum’s pension.

How old is your mum? Is her pension a “money pension” or is it linked to her last salary?

Samantha says

Hi thank you so much for your response apologies for not being able to get back to you

We are allowed to stay as long as we like, we contribute to household costs and split broadband costs etc

We were wanting to move out but I’m not longer sure if that would be a viable option due to my health issues and now being on ESA and a disability benefit.

My mum is currently 54 but she will be 55 in July, I believe it was linked to her salary? the pension was provided through the NYCC themselves when my mother was employed by them, she no longer works for them and she no longer pays anything into it as the contributions would be taken out of her salary monthly.

If it helps we live in the UK and hers would be classified as an Employer’s Pension

Sara (Debt Camel) says

In that case I think you should both talk to National Debtline about your options, they can look at your incomes and expenses in detail – phone 0808 808 4000.

Your mum’s pension pay not be a problem at all, but as she is coming up to 55 it would be better to get advise immediately, not delay.

Mr J M says

Hi. Would like some advice please. I’m 67yrs old. Have a low pension of just under £600 per month. My wife is also a pensioner , plus she is disabled. I am not disabled but do have health issues. I carried on working as a bus driver and when covid came a long I was furloughed, more because of the danger to my wife as she has a lung problem and is on oxygen 24/7. I was working a 3 day week and my pay reflects that. I’ve been furloughed for the past year and have kept up minimum payments on the 4 credit cards. None of them are maxed out. Hardly used them at all for a couple of years. I’n not interested in ripping the banks off and I know I’ll never be able to pay them off. I don’t want to go back to work now. I’ve had the job for 24years and hated most of those years. It feels like I’ve wasted a 3rd of my life. I don’t have any savings. Don’t own my own house. I’m still on furlough so I’m using my pension to pay my debts. The furlough is coming to an end. I don’t want to go back. My wife is very ill and needs me at home more and more. When the furlough money finishes, I’ll need my pension for the essentials of living. I’m never going to be in a position to pay the bank debts off. What can I do?

Sara (Debt Camel) says

I think at 67 it is time to stop work you don’t like!

Can I ask what your housing situation is?

can you say what the credit cards add up to?

do you own a car?

Mr J M says

We live in a rented housing association house.

The credit cards add up to approximately £8000.

I have a car which I is on HP until August but I can’t sell it after that because of regular hospital visits for my wife and she is unable to use public transport and Taxis arn’t too happy with wheelchairs and oxygen tanks. and also the oxygen tanks have limited time so the car is essential for her.

Sara (Debt Camel) says

I think you need to talk to a debt adviser, but it won’t be possible to make a final decision about your debt options until you know what your income will be when you have stopped work. And after August you will have more “spare income” as your car will be paid for.

Assuming that your decision to stop work is final (and with your wife’s health on top of your age and the fact you don’t enjoy the job it sounds it – but this is your decision, no-one else can say what you should do), then probably the best order is to:

– hand in your resignation

– talk to your local Citizens Advice about benefits. If your wife is not getting disability benefits, she may be entitled to them.

– also talk to Citizens Advice about your debts.

It may be you can afford a debt management plan where interest is frozen on your debts. Otherwise a token payments plan is a possibility (as the article above suggests).

Mr J Martin says

The car is an 11 year old Toyota Prius. Not worth a lot.

Sara (Debt Camel) says

ok, then in that case it is possible you may qualify for a Debt Relief Order – Citizens Advice can help you look at this too.

Mr J Martin says

Hi Sara.

This is just to update you on my situation. I talked to National debtline and did some research and in the end decided to write to each of my creditors and explain my situation. They were all surprisingly very approachable and all were very helpful. My situaion is a bit unique because I’m retired so sadly it’s not the same route to go for all the people with financial problems. I showed them all my budget and also added a seperate page breaking down the budget for easier understanding. Anyway, now, a few months on, I am paying 4 creditors £1.00 each per month and the other 2 have kindly wiped the debt. One was for £2700 and the other debt cleared was just £230.

Thank you for your help and advice.

Sara (Debt Camel) says

good result for you!

Noel says

Hi

I’d used national debt line’s budget calculator and it showed after paying priority expenses I’m left with a negative value

1. Will IVA not be applicable due to the negative value? Will it be the same with DMP?

2. I might be able to spare £1 payment for the 9 creditors. How will these affect me about my mortgage especially for a new fix happening next year?

3. Due to the large amount of loan and the increase of new fix the £1 token payment might stay long. What will be the consequences of being in this situation?

Sara (Debt Camel) says

This is now? or when your mortgage goes up next year? How large a negative amount?

Noel says

Plus will I still be able to secure a new fix even by paying £1 token?

Item 2 meant will I be forced to use equity release or other options to pay into that unsecured debts?

The negative amount will be £200 next year. So I’m looking for £1 token payment plus affordability claims on old CC.

Please share me where to post questions on affordability.

Plus add the HTB payment

Can they petition for bankruptcy? If so how is the process?

Sara (Debt Camel) says

so you are OK at the moment but will be more than £200 down a month after the HTB payments are factored in.

answering your questions:

“Will IVA not be applicable due to the negative value? Will it be the same with DMP?”

Correct. You have NO spare money to pay either. It would be madness to sign up to an IVA, and you probably wouldnt be offered one by any reputable firm.

“I might be able to spare £1 payment for the 9 creditors. How will these affect me about my mortgage especially for a new fix happening next year?”

You should still be offered a new mortgage fix. And the token payments you will have to make aren’t relevant for that as you are currently paying an affordable DMP.

BUT you need to consider how long a fix to take. What is the chance of this solicitor being able to recover some of the money you were scammed out of? If it isnt a reasonable chanmce, you should seriously consider your other options eg selling the house. If you take a 5 year fix and then are forced to sell anyway, that will just decrease the equity you are left with as an early repayment change will be added.

“Due to the large amount of loan and the increase of new fix the £1 token payment might stay long. What will be the consequences of being in this situation?”

Your creditors may be more likely to consider going to court for a CCJ. And then getting a charge on your house.

“Item 2 meant will I be forced to use equity release or other options to pay into that unsecured debts?”

Equity release is only relevant in an IVA which does not look like a feasible option for you. A CCJ and a charge over you house is unusual, but given that some of your debts are very large cannot be ruled out.

“Can they petition for bankruptcy? If so how is the process?”

that would be much more unusual than a CCJ and a charge over your house as your creditors are all normal consumer credit act lenders. It can’t be totally ruled out thought given your extremely large loan. See https://www.citizensadvice.org.uk/debt-and-money/debt-solutions/bankruptcy/creditors-making-you-bankrupt/creditor-trying-to-make-you-bankrupt/. This is not something that is an immediate problem but this comes back to how likely you are to get any money back from the scam.

“Please share me where to post questions on affordability.”

here for credit cards: https://debtcamel.co.uk/refunds-catalogue-credit-card/

BUT given the scale of your problems, you should not think that affordability complaints can do more than make minor improvements – they will not really change your issue.

Let me be clear.

If you had not lost c £75k to a scam, you would still be facing a massive problem next year when your mortgage rate goes up. The £200 negative budget, plus more for the HTB segment, would still be there even if you had no other debts at all…

You have bought a house you cannot possibly afford at higher interest rates.

Selling the house has to be a serious option for you.

Why not phone National Debtline and talk through all your options, including the ones you don’t like?

Ryan says

Hi, I was rejected by one of my creditors for an IVA and have been forced to go down the bankruptcy route. I have now been told my job will cease to be at the end of the year and will have a payout. This will all be taken by the OR as per the terms, as it will be paid during bankruptcy but before the 12 months is up.

With this in mind, would it be better for me to deal direct with creditors or debt collection agencies, who will offer a 50% reduction as one off payment to settle the debt?

I really cant have no job and also nothing there to fall back on being sole earner in my home.

Thanks

Sara (Debt Camel) says

Sorry this is not an option for you once you have gone bankrupt.

(You probably wouldn’t have been any better off in an IVA either.)

Ryan says

Thanks Sara,

Sorry i wasn’t clear, i haven’t submitted the bankruptcy application just yet – so thinking it may be easier to deal with credit agencies than original creditors?

Sara (Debt Camel) says

ah! That is a massive difference.

How large are your current debts? Are you making normal payments, a variety of payments arrangements or what?

are you buying or renting? do you have a car on finance – if so is it HP or PCP?

how much do you expect to get from the redundancy?

how easy do you expect it will be to get a new job?

Ryan says

35k Debts

Not paid anything in 3 months since my IVA got rejected – most have hold on interest – few have gone to DCA already

Renting

No car on finance – own one worth 2k

Expecting just over 30k redundancy – which is tax free

Jobs not that well come where i live and certainly wont be of the level i am used to – which was enough just to cover bills/house etc etc

Sara (Debt Camel) says

did you have one very large creditor?

Ryan says

One is double the next highest debt, it was them who rejected the IVA also.

Total about 10/12 creditors, raging from £150 to 8.5k

Sara (Debt Camel) says

So your problem isn’t the debts, it’s the fact that a new job may not pay enough to cover the bills and essentials?

I think your priority has to be job hunting and thinking whether you need to move.

You can offer the creditors a small monthly payment, possibly a token £1 payment, at the moment. Until you get any redundancy money what other option do you have? Then if you do lose your job, you have the redundancy money as a cushion if your new wage is too low.

You could also look at making affordability complaints against all the debts now – see https://debtcamel.co.uk/tag/refunds/. In this situation the more you can the debts reduced the better!

I think you should talk to National Debtline on 0808 808 4000 about your options here. They have a template letter to offer £1 a month if they feel that is an appropriate option at the moment.

K says

Hi Sara,

I wasn’t able to make payments towards 5 credit cards in 2018, subsequently ended in defaults and closed accounts. I haven’t taken credit out in the last 6 years and have been paying these creditors £1 each a month with step-change ever since (been a student for 4 years). I have noticed all accounts have now dropped off my credit score on all the major credit score companies. What do I do here? keep paying the £1 until I get a job then start paying bigger amounts? Stop paying the £1? and is there still a chance they can give me a CCJ? I want to be able to get a mortgage and credit in the future.

Sara (Debt Camel) says

when does your course end? How large are these debts at the moment?

K says

I graduate next May. I currently owe £14.5k.

Sara (Debt Camel) says

Ok so the debts will have dropped off your credit records when it was 6 years from the default date.

But you are still making payments each month to the debts, so they will never become “statute barred” – to old to be be taken to court for. So if you stop paying, you are very likely to be taken to court for a CCJ. the fact they arent on your credit record is irrelevant

So your choices are:

1) carry on paying £1 a month – the problem with this is at some point the debt collectors (I guess they have all been sold to debt collectors by now?) may ask you to pay more then you are earning. And still paying these debts will make it very hard to get a mortgage – the mortgage lender will know these are old defaulted debts as they will be able to see who you are paying from your bank records

2) increase the monthly payments when you are earning – it depends how large your income and expenses will be. For most people just starting on a career 14k of debt is a lot and will make it hard to save a deposit for a mortgage at the same time

3) make settlement offers to the debts – the debt collectors would probably accept low offers now, but where would you get the money from? Don’t borrow to make settlement offers – that is getting new, expensive debt in exchange for old debt at no interest and off your credit record.

4) ask the current debt collectors to produce the CCA agreement for the debts. See https://debtcamel.co.uk/ask-cca-agreement-for-debt/ for more about this. It isn’t guaranteed to work for any debt. If you try this it is best done now, as the debt collectors may ask you for your current income & expenditure to check you cant pay more then £1 a month.

5) carry on paying £1 a month for as long as possible but save up some money to make settlement offers with.

K says

Thank you so much for your thorough reply. I will think carefully about which route I choose to go down.

nina louise says

Hi Sara,

I am currently helping a family member with some debt issues they are facing. Lets call this person L.

L is in around £17,000 worth of debt with credit cards and loans. not including a HP car finance still owing around £4,300.

L has no savings and no valuable assets.

L is facing some financial hardship and although is maintaining monthly repayments they cannot continue to do so. and needs to consolidate all loans, card and phone contracts totalling to the above figure of around £17,000

We initially were going to apply for an IVA but now its looking as the worst option.

what would be the best option possible for L?

i have been looking into a DRO but not quite sure how this works? do you make a monthly repayment?

with any debt management plan is there a way of keeping certain creditors e.g. L has an account with PayPal and uses regularly and wouldn’t want to loose this account is there a way of keeping this and obviously the car?

ideally L would like to consolidate debt of around £17,00 keep the car hp which is £109 PCM and there paypal account open.

what do you recommend

thanks

Nina Louise.

Sara (Debt Camel) says

With no assets, an IVA isn’t likely to be a good option for them.

How much is the car worth now?

nina louise says

Hi Sara, Retail value is around £2800-£3000.

if an iva isn’t a good option what would you recommend? said persons cant financially afford to pay there bills and are living month to month constantly using credit cards and overdrafts to get by.

thanks

chanel

Sara (Debt Camel) says

Ok with a car value under 4K a DRO may be possible.

In a DRO you dont make any monthly payments.

Paypal is very expensive – she needs to stop using it in any option. When the other debts are gone/being cleared with an affordable amount she should be able to put aside money monthly for clothes and gifts so she no longer needs that sort of credit.

I suggest she talks to StepChange and see if they recommend a DMP or a DRO. She should complete their income & expenditure form and think about what she needs to spend long term, not how little she can get away with for a month or two. So include amounts for Xmas, dentist, haircuts, clothes , say Yes to savings etc https://www.stepchange.org/

Nina louise says

Hi Sara,

Thanks for your response.

I’ll get hold of step change to.

So just to confirm with a dro, you add the bills that you want to consolidate but you pay no monthly fee and then it gets wiped off after a year? This seems almost onto be true?

Thanks

Chanel

Sara (Debt Camel) says

yes. “Consolidate” is a misnomer here – a DRO is a form of insolvency that clears your debts like bankruptcy and an IVA.

Nina louise says

Ok great, sorry I just want to make sure I’m correct here, so with a DRO you make no monthly payments and after a year all debt is wiped and the dro remains on the credit file for 6 years?

Sara (Debt Camel) says

yes that is right